Financial markets are always in flux and constantly evolving, making the work of a successful investor at best interesting and rewarding and at worst stressful. The trick is recognizing how the ebb and flows of daily action can be a tactical opportunity or just noise and how the long run might actually be impacted by the short run. In today’s blog, we tackle a few topics that zoom on the long run – short run spectrum in an effort to provide a few interesting datapoints about tactical opportunities and long-term view of markets.

The Long View

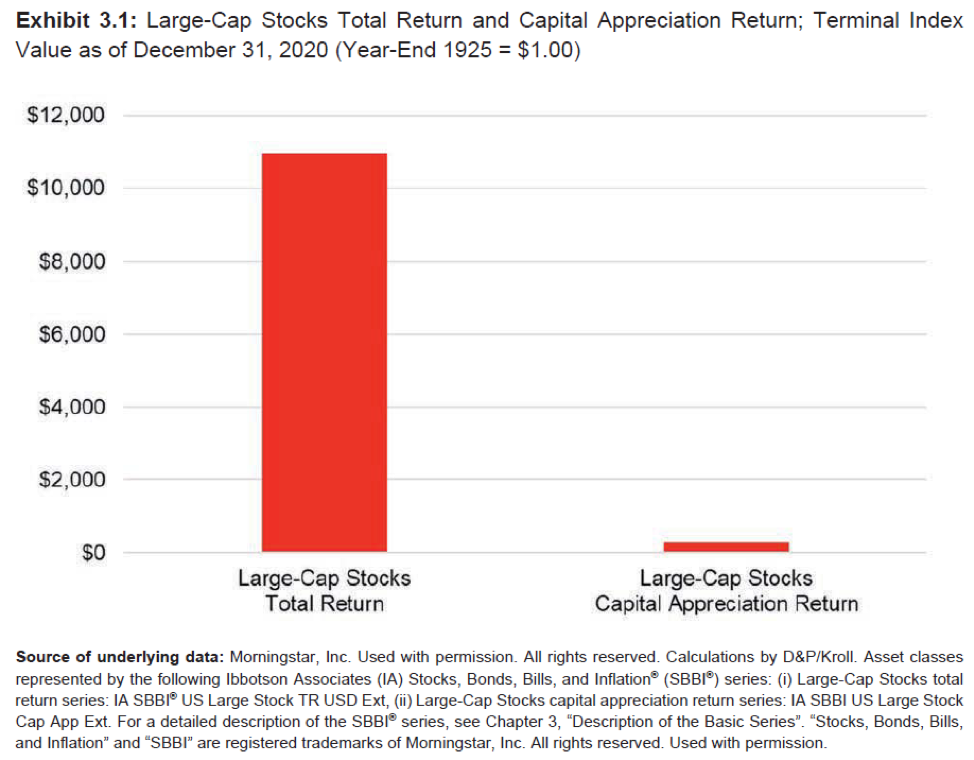

The CFA Institute, along with Morningstar, has recently published the yearly “Stock, Bonds, Bills and Inflation” report (SSBI), a 200-page volume filled with interesting statistics about markets. For the geeks at heart is like Xmas… Some findings are worth pointing out as they reinforce, and quantify, well known market tenets. The SSBI report shows how small caps maintain a return advantage over large caps in spite of the recent outperformance of bigger companies (namely tech large caps). In the historical period from 1925 to 2020, small caps have produced a return four times bigger than large caps. Another reinforcement comes from a review of returns when they include dividend reinvestment versus a no-reinvestment approach. Since a picture is worth a thousand words, we think the best way to prove the magnifying effect of a dividend reinvestment strategy is to show the actual SSBI chart:

The third and probably more accepted statistical tidbit relates to the outperformance of stocks over cash and bonds. Based on the SSBI report, equities beat cash 69% of the times in any 2-year period, all the way to a 91% success rate over a 10-year period. Surprisingly, it is not a 100% sure win, a fact that stresses the importance of sset allocation and tactical adjustments.

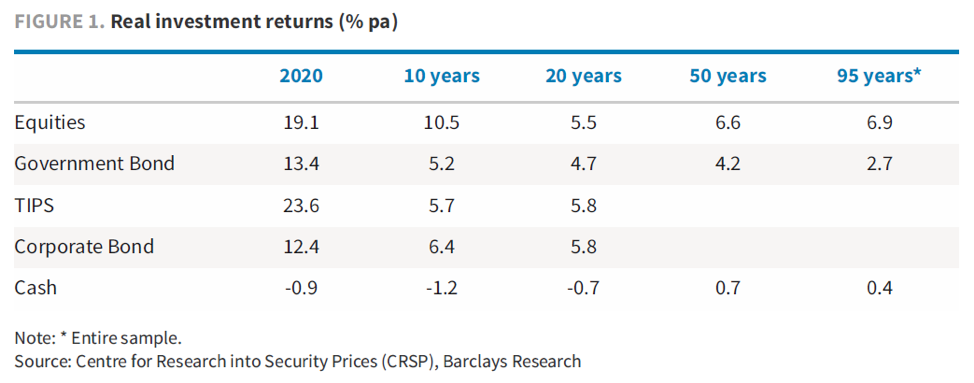

The following is a table showing real US returns over different time periods for stocks, Treasuries, cash, and corporate bonds. While the equity outperformance is pretty clear and consistent, the last 20-year window blurs some of the lines, once gain suggesting a need for good asset allocation modeling.

The Tactical View

From a tactical perspective, the analysis must focus on the rise and possible persistence of inflation. After decades of lower inflationary pressures, the convergence of easy monetary policy, increased fiscal policy, COVID related production bottlenecks and years of under-investments in commodities are now reversing the previous trend in prices. While everyone agrees that we are going to (and already are in some markets such as housing and energy) experience rising prices, there is a lot less consensus on whether this phenomenon will be transitory or long lasting. While it is difficult to envision 1970s type of pricing pressures due to different demographics and different industrial processes, it may also be too optimistic to think that the perfect storm that is awakening prices might just be resolved very quickly.

From an investment management perspective, it is likely that most portfolio managers would shift allocations as an insurance policy, whether or not they feel strongly about persistent rising prices. Energy (old fashion and new tech), value strategies and specific commodities (i.e. copper) should continue to see rising money flows.

The Trading View

The two recent announcements in the media sector – AT&T spinning off its media portfolio to merge with Discovery and the Amazon acquisition of MGM – are indicating the increasing opportunities to get active in the reshaping of the media landscape. Shifting consumer tastes, new technologies and new strategic alliances are going to provide fuel to M&A activity for quite some time. We have been involved actively with Viacom and CBS (now one company again) since over a year ago and with AT&T more recently. We will continue to monitor the sector for more action.

Please call our Team, should you want to discuss any of these topics in more details.