State of Play: A Few Yards Left

In this volatile and largely disappointing 2022, we have a few yards left to go before closing the books and realign for a new twelve-month cycle.

There is a few good news to carry us into Xmas, such as the usually positive seasonality and some positive stats on public enemy number 1, inflation. Jay Powell, in his latest press conference, sent mixed signals as he indicated a slowing of the pace in raising rates, but he also indicated that the peak rate will probably be higher than expected (north of 5%?) and that we may linger for a bit longer at those altitudes. Powell also clearly stated that he would rather take the risk to overtight and then clean up the mess afterward rather than be too soft now and risk a structural entrenchment of inflation expectations.

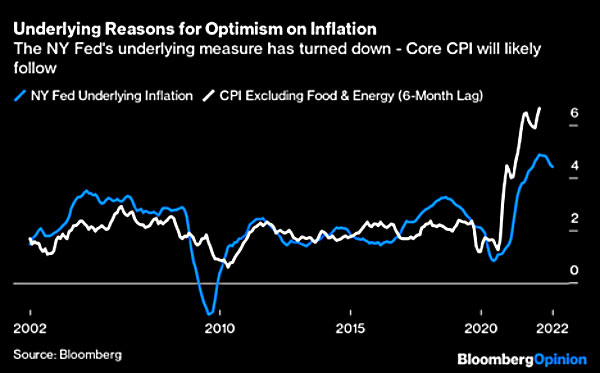

However, just after Powell’s conference, unemployment number showed an uptick, which is not good news for those losing their job, but it’s certainly good news from a monetary policy perspective. Additionally, John Authers at Bloomberg shared a chart today from the NY Fed showing that their proprietary “underlying inflation” metric has started to significantly diverge from CPI and began a downtrend. Authers quotes that the last time the two indexes had such a spread, CPI collapsed within nine months.

Recently, we also reviewed updated numbers from the ISM Manufacturing Price Index which is showing a downtrend as well.

At this point, despite the rhetoric, we might start to see a more flexible Fed, more conscious of the underlying weakening of the economy.

This new paradigm, along with much higher yields than when we started the year, it probably opens the door for a reasonable approach toward increasing duration in bond portfolios. It would also seem to usher in a renewed negative correlation between bonds and equity for 2023, a much-needed change for successful portfolio construction.

SECTOR FOCUS: Small Cap Biotech

It was a bad year overall but certainly miserable for small biotechs. An oversaturated sector spent the last twelve months readjusting valuations in a crowded field while dealing with increasingly higher cost of financing. The sector corrected significantly and started to turn around in summer. An interesting study from 2016 (source: biopharmacatalyst.com) shows that if an investor bough into XBI since its inception, he/she would have been in a 10% drawdown 51% of the time and in a 20% drawdown 25% of the time. However, such an investor, would have gained a 257% return over the next decade equal to a compounded yearly return of 13.7%.

Beyond history and stats, there are also some fundamental reasons that may fuel the sector turnaround. M&A deals are beginning to occur, and we expect large pharma companies to continue to refresh their pipelines by looking at patents and research produced by small labs.

We also note that while the most recent money flows are negative to the tune of $5 billion being withdrawn by investors, the one-year flow remain surprisingly positive at $2.4 billion.