In a previous analysis posted in 2016, we stressed the importance of dividends in the growth of a portfolio. Equity dividends are consistent cash payouts, from companies to shareholders, that historically have grown at an average pace way superior than the rate of inflation. Even during long periods like the “lost decade” for equity returns between 2000 to 2009, dividends grew in a healthy way.

The persistent environment of low yields from bond investments has emphasized even more the importance of incorporating a dividend strategy in a wealth building portfolio. In fact, the low yields provided by bonds has been pushing not only younger investors but also retirees toward high dividend paying equities to fund their income need.

As of December 31st, 2018, 39% of stocks included in the SP500 had yields higher than the 10-year US Treasury bond (source: Ned Davis Research). In the past, this situation was generally inversed, with US Treasuries usually sporting a better yield than the average dividend pay-out. Even compared to corporate bond yields, things look interesting as equities pay similar yields but with a growth rate in excess of inflation while corporate bonds are fixed coupon instruments.

Dividends are not just a superior source of income but for those investors that do not need the cash-flow and therefore have the option to reinvest the pay-out into shares, dividends have the power to turbo-charge the total return of a portfolio. The power of dividends and their compounding is illustrated in this chart which shows the drastic difference in total return between a hypothetical account that includes price return only and one that incorporates dividend reinvestments.

(source JP Morgan)

In choosing the right dividend paying stocks, one needs to go beyond the pure percentage distributed because very high dividends are often a red flag of something amiss with the company. One must look for sustainability of cash-flow and a pay-out ratio (the amount of money paid out to shareholders as a percentage of earnings) that is not too high. This is required in order to avoid dividend cuts when an economic correction suddenly reduces the ability of the company to produce free cash-flow. Quality and type of assets is also of concern as pay-outs can occasionally be subsidized by sales of asset.

High dividend paying stocks can be found in different sectors. REITs are a popular choice as they run a business model highly focused on cash-flow generation and pass-through payments. Utilities are similar, even though their dividends are often much lower than real estate companies. However, the sector is currently showing fairly high valuations. Energy stocks have the best yield at the moment, the result of historically low valuations and a streamlining of balance sheets which was dictated by the oil crash of 2015. Financials are also attractive in dividend terms, in light of their renewed ability to grow distributions after the post financial crisis impairment.

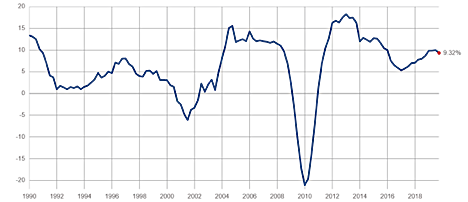

As mentioned in our introduction, one extremely positive characteristic of dividends is their rate of growth over time. In the following chart, one can see the year-over-year growth rate for dividends of the SP500. Going back to 1990, the mean growth percentage has been 6.07%, the median rate 6.80%.

(source: Standard and Poor’s)

In conclusion, in a world of consistently low bond yields, one cannot dismiss the importance of dividends to fund retirement and lifestyle.